India today has highest number of young employees joining the work force globally. Starting your first job is an exciting milestone. With your first pay cheque comes a sense of independence — and also the responsibility to build good financial habits early. The choices you make now can lay a strong foundation for your future financial well-being. Here are 9 practical saving tips for new employees that can help you turn your earnings into long-term wealth.

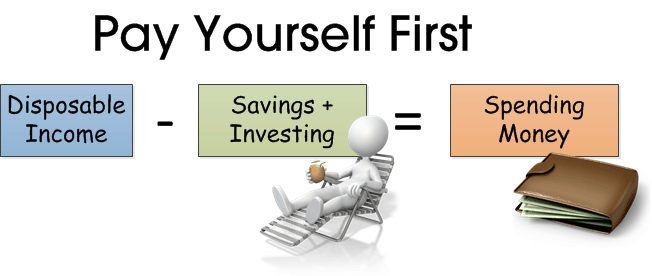

1. Pay Yourself First

Before spending on lifestyle upgrades, make it a priority to save a portion of your income. A good thumb rule is to set aside at least 20-30% of your salary the day it hits your account. Automate this through systematic investment plans (SIPs) in mutual funds or direct transfers to savings/investment accounts.

2. Create an Emergency Fund

Life is unpredictable. Build an emergency fund equal to at least 3-6 months of living expenses. Park this in a liquid or ultra-short-term debt fund, or a high-interest savings account. This cushion will protect you from unforeseen medical, job, or personal crises.

3. Avoid Lifestyle Inflation

It’s tempting to upgrade your phone, car, or wardrobe once you start earning. But overspending can derail your savings goals. Learn to differentiate between needs and wants. Remember — what matters is growing your wealth, not keeping up with peers.

4. Start Investing Early

Thanks to the power of compounding, the earlier you start investing, the less you need to save to build a big corpus. Even small SIPs in diversified mutual funds or index funds can grow substantially over the years. Time in the market beats timing the market.

5. Don’t Ignore Insurance

Insurance is not an investment — it’s protection. Ensure you have adequate health insurance even if your employer provides a group policy. If you have dependents, consider term life insurance. Buying young means lower premiums.

6. Minimise Debt

It’s easy to fall into the trap of credit cards and personal loans. Use credit responsibly, pay off dues in full, and avoid high-interest debt. Building wealth is much harder if a large chunk of your salary goes towards EMI repayments.

7. Set Clear Financial Goals

Whether it’s higher education, a home, travel, or early retirement, define your goals. Having clear targets helps you choose the right investment strategies and motivates you to stay disciplined.

8. Save on Taxes

Explore tax-saving options like ELSS mutual funds, PPF, NPS, and EPF contributions. Not only do they reduce your tax liability under Section 80C, they also help you build long-term assets.

9. Review Regularly

Your income, expenses, and goals will evolve. Make it a habit to review your budget, savings, and investments at least once a year. Adjust your plan as needed to stay on track.

Final Word

The best time to build sound financial habits is when you start earning. Small, consistent efforts today can help you achieve financial freedom tomorrow. Remember: it’s not about how much you earn, but how wisely you manage what you earn.

Happy Investing.