We diligently track our daily health metrics on our smartphones — counting steps, monitoring calories, and analyzing sleep cycles. Yet, when it comes to our overall financial health, many of us are surprisingly flying completely blind. A common refrain I hear from successful professionals across the country is, “I earn a substantial salary, but I have no idea where my money goes each month, or what I actually have to show for years of hard work.” In an era of seamless digital payments, it has become incredibly easy to lose track of daily spending. This deep-seated financial anxiety rarely stems from a lack of income. Instead, it arises from the absence of a simple diagnostic tool: a personal financial statement.

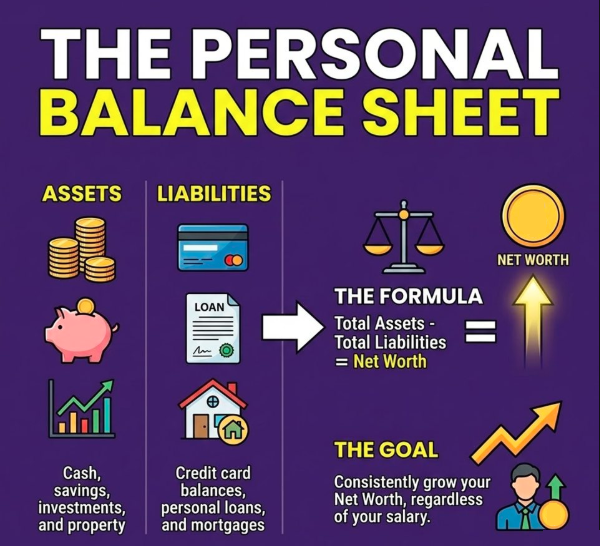

Just as a publicly listed company publishes a balance sheet every quarter to offer absolute transparency to its shareholders, an individual must have a clear, uncompromising picture of their own financial standing. A personal financial statement serves precisely as your individual balance sheet. It is a straightforward document that meticulously lists your assets and your liabilities. Assets encompass everything you own that holds value, such as savings accounts, real estate, provident funds, and market investments. Liabilities represent what you owe to others, including home mortgages, vehicle loans, and outstanding credit card balances. The mathematical difference between what you own and what you owe represents your true net worth.

In the Indian context, our financial lives are frequently a complex emotional mix of traditional wisdom and modern financial instruments. A typical middle-class household across the nation might proudly hold physical gold, ancestral property, fixed deposits, and market-linked instruments. Creating a personal financial statement forces you to consolidate this highly fragmented picture into a single, cohesive dashboard. It helps you instantly realize if your wealth is overly concentrated in illiquid physical assets that generate no regular income, or if high-interest personal debt is quietly eroding your hard-earned wealth behind the scenes. More importantly, it profoundly shifts your mental focus from merely saving what happens to be left of the monthly salary to actively building and protecting your long-term family net worth.

Documenting this reality on a simple spreadsheet can be a profound financial revelation. It clearly dictates whether you have adequate liquidity to weather unexpected emergencies and whether your long-term retirement and children’s education planning is genuinely on track. This foundational bedrock effectively removes the stressful guesswork from your life, replacing vague hopes with concrete data. As you utilize this living document to map out your journey and explore various avenues to grow your assets, it is crucial to remain grounded about the long-term nature of wealth creation. Please remember that investments in mutual funds are subject to market risks.

Because past performance may or may not be sustained in the future, projecting historical market behaviors onto your future net worth can be misleading. Every individual should have a unique personal balance sheet and distinct risk appetite, which is why investors should consult their financial advisor before making investment decisions to ensure every step aligns seamlessly with their true financial reality.