In my two decades of advising families and young professionals, I’ve realized that most financial mistakes are not caused by lack of intelligence—but by misconceptions. Money is one of those subjects everyone has an opinion about, but few take the time to understand deeply. Getting your personal finance fundamentals right is less about complex strategies and more about unlearning the myths that quietly drain your wealth.

The first misconception is that earning more automatically means becoming wealthy. Many assume that a higher salary guarantees financial freedom. In reality, it is not income but disciplined saving and investing that builds wealth. Without a plan, lifestyle inflation swallows every raise. I’ve seen individuals earning ₹30 lakh a year with no corpus, while others earning half that amount own homes and have steady retirement funds. Wealth creation is not about what you earn—it’s about what you keep and how you grow it.

Another common belief is that insurance is an investment. It isn’t. Insurance is a protection tool, not a wealth-creation vehicle. Mixing the two often leads to not only poor returns but also inadequate coverage. The truth is, term insurance offers pure protection at minimal cost, while investing in equity mutual funds or index funds builds long-term wealth. Understanding this distinction is one of the biggest steps toward financial maturity.

Many investors think they are risk averse, they let their money lie in their savings accounts or at best invest in fixed deposits. But in a country where inflation averages 6-7%, these low-yielding investments loses purchasing power every year. Not understanding market volatility & it’s mitigation allows inflation to silently erode your wealth. Equity, when held through diversified funds for 10 years or more, has historically beaten inflation comfortably. The longer your horizon, the lower your risk.

Then there is the myth that buying a home is always better than renting. Emotionally, ownership feels comforting, but financially, it depends on affordability and flexibility. If a large portion of your income goes toward EMIs at the cost of investing, you might end up house-rich but cash-poor. Real estate can be a good asset, but only after you’ve secured your emergency fund, insurance, and long-term SIPs for children’s education, retirement, etc…

Another misconception is that loans are harmless if EMIs are affordable. The truth is, EMI culture has trapped millions into spending tomorrow’s income today. Every EMI delays financial freedom. Before buying the latest phone or car on credit, ask yourself: is it an asset appreciating in value, or a liability you’ll keep paying for long after the excitement fades?

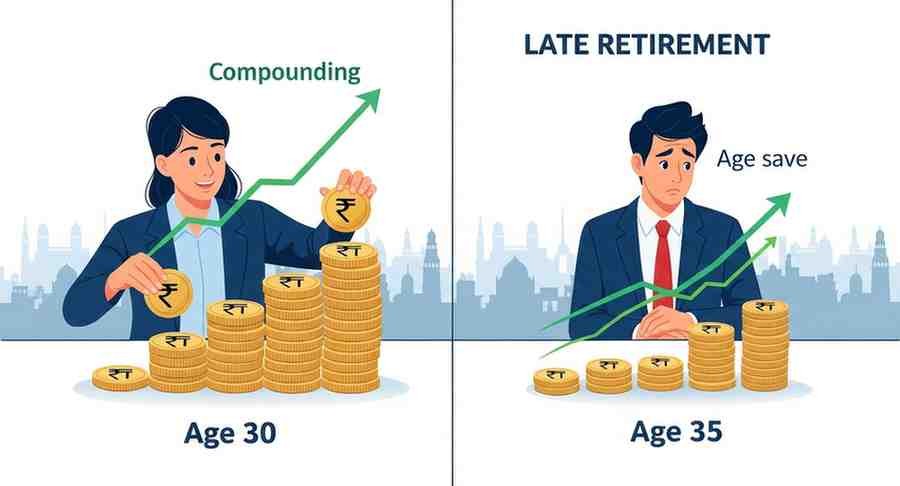

Finally, many people believe that retirement planning can wait. But compounding rewards only those who start early. A 25-year-old investing ₹10,000 a month for 20 years at 12% will accumulate ₹1 crore; he delays by 10 years, they’ll have barely half that. Time, not timing, is the real secret.

The truth about money is simple but powerful: spend less than you earn, insure adequately, invest regularly, avoid unnecessary debt, and let compounding work quietly. Financial prudence isn’t about deprivation—it’s about freedom. The sooner you replace money myths with financial truth, the faster you move from working for money to making money work for you.