When Amit received his annual bonus, he felt a familiar rush of excitement. It was nearly three months’ worth of his salary—something he had worked hard for all year. Within days, plans started forming. A new phone, a short vacation, upgrading his car, and a celebratory dinner with friends.

“It’s my reward,” he told himself. “I deserve it.”

A month later, the bonus was gone. Not wasted—just spent. And yet, strangely, the satisfaction had faded much faster than the money.

A few weeks later, Amit met his friend Neha over coffee. She too had received her bonus.

“So, where did yours go?” Amit asked casually.

Neha smiled. “Part of it went into a trip, yes. But most of it—I invested.”

Amit laughed. “You always do that. Don’t you feel like enjoying your money?”

“I do,” she replied calmly. “But I also want my money to work for me.”

Seeing Amit’s curiosity, she continued. “Let me show you something.”

She pulled out her phone and opened a simple investment tracker.

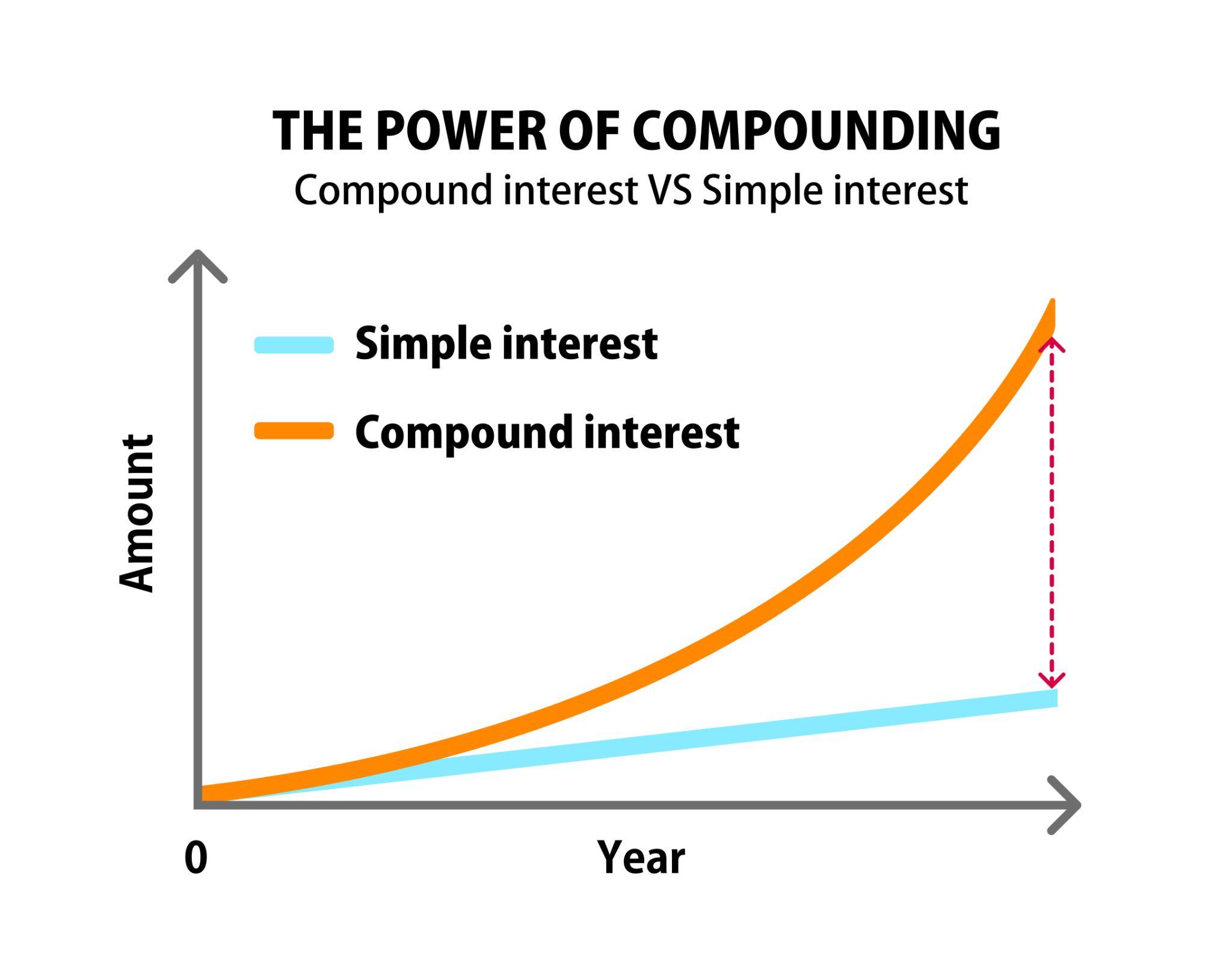

“Five years ago,” she said, “I started investing my annual bonus into mutual funds. Nothing fancy—just consistent investing. No timing the market, no chasing trends.”

Amit glanced at the screen. The numbers had grown far more than he expected.

“That’s compounding,” Neha explained. “The first year feels slow. The second year doesn’t feel very different. But over time, your returns start earning returns. That’s when things change.”

Amit leaned back. “But what about enjoying life today?”

“Of course,” Neha said. “I’m not saying don’t spend. I’m saying don’t spend everything.”

She paused and added, “The problem with bonuses is psychological. Salary is routine—we respect it. Bonus feels extra—we spend it. But if you treat your bonus as an opportunity rather than surplus, it can change your future.”

Amit thought about it. Every year, his bonus disappeared quickly, while his monthly expenses felt more controlled.

“So what should I do differently?” he asked.

“Simple,” Neha said. “Decide before the money comes in. Allocate it. Spend some, invest some. Don’t let emotions decide for you.”

She continued, “Let’s say you invest even 50% of your bonus every year. Over 10–15 years, that alone can build a meaningful corpus. Not because of high returns, but because of consistency and time.”

Amit nodded slowly. “So the real difference is not how much you earn, but what you do with it.”

“Exactly,” Neha smiled. “Instant gratification feels good for a moment. Compounding feels invisible at first—but powerful over time.”

That evening, as Amit reviewed his finances, he realised something simple yet profound. His salary sustained his present. But his bonus had the potential to build his future.

The next year, when his bonus arrived, he made a different choice. Not a drastic one—just a deliberate one.

He spent some. And he invested the rest.

Because sometimes, the smartest way to enjoy money is not just to spend it—but to let it grow.