The world of investing has never been more accessible. With a smartphone and a few clicks, investors can access stocks, mutual funds, insurance products, and a multitude of investment opportunities. While this democratization of finance is a positive development, it has also created fertile ground for mis-selling, misinformation, and poor financial decisions.

As a wealth manager, I often find that investors don’t lose money because markets fail them. They lose money because they fall into behavioural and financial traps that divert them from long-term wealth creation.

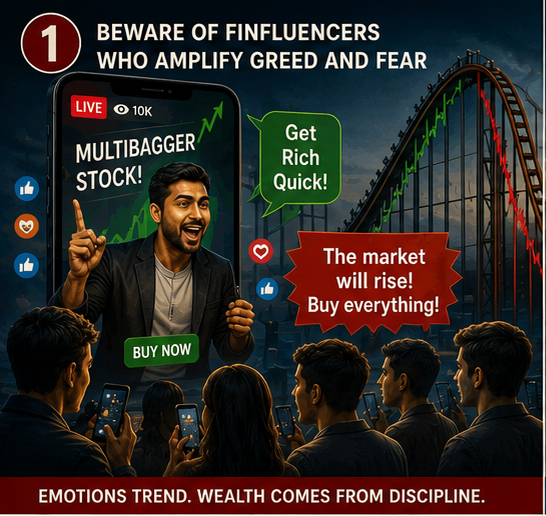

1. Beware of Finfluencers Who Amplify Greed and Fear

Social media has created a new class of financial influencers, commonly called “finfluencers.” While some provide valuable educational content, many thrive on sensationalism. During bull markets, they amplify greed by promoting quick wealth stories and “can’t-miss” opportunities. During corrections, they magnify fear by predicting crashes and economic doom.

The problem is that emotional content attracts attention, but rarely helps investors build wealth. Long-term investing requires patience and discipline, not constant reactions to trending videos or market predictions.

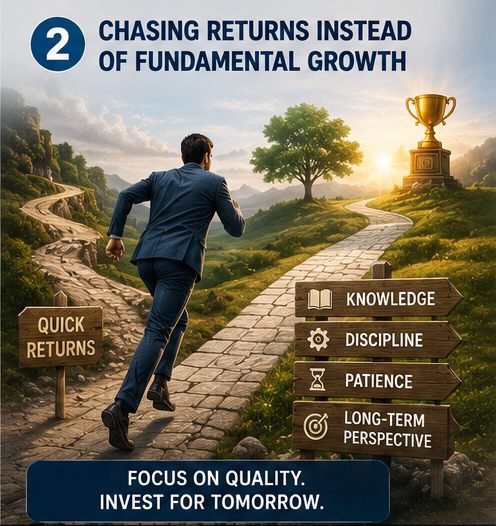

2. Chasing Returns Instead of Fundamental Growth

A common mistake is investing based solely on recent performance. Investors often rush into the best-performing fund, stock, or asset class after seeing impressive returns.

Unfortunately, yesterday’s winner is not always tomorrow’s winner.

Instead of asking, “What return did this investment generate?” investors should ask, “What businesses or assets am I investing in, and does the investment align with my long-term objectives?” Sustainable wealth is built by participating in fundamental growth, not by chasing temporary performance leaders.

3. Investing Without Understanding the Product

Many investors purchase products they do not fully understand. Whether it is an insurance policy, a thematic fund, a structured product, or a leveraged investment, confusion often leads to disappointment.

Before investing, every investor should be able to answer three simple questions:

What am I investing in?

What are the risks?

How does this fit into my financial goals?

If the answers are unclear, the investment probably deserves further evaluation before committing money.

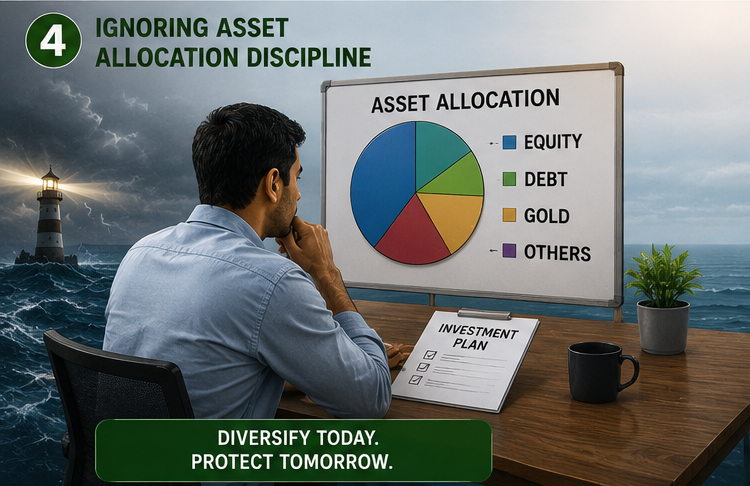

4. Ignoring Asset Allocation Discipline

Asset allocation is one of the most powerful drivers of long-term investment outcomes. Yet many investors abandon it during periods of market excitement.

When equities rally, portfolios become equity-heavy. When markets fall, investors suddenly seek safety. This constant shifting often destroys value.

A disciplined allocation across equity, debt, gold, and other suitable assets helps manage risk and reduces emotional decision-making. Successful investors do not predict market cycles perfectly; they prepare for them through diversification.

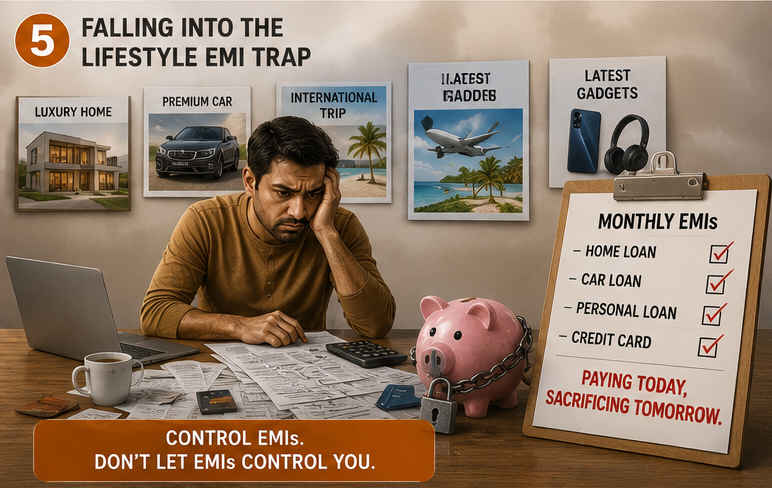

5. Falling Into the Lifestyle EMI Trap

Perhaps the most overlooked trap isn’t an investment product at all.

Larger homes, luxury cars, international vacations, and the latest gadgets are increasingly financed through easy EMIs. While each EMI may appear manageable individually, together they can severely limit an investor’s ability to save and invest.

Many households today earn well but accumulate little wealth because future income has already been committed to lifestyle expenses.

The biggest threat to wealth creation is often not market volatility but poor financial behaviour. In investing, avoiding mistakes is often more important than finding the next big opportunity. Sometimes, protecting wealth begins with learning what not to buy.