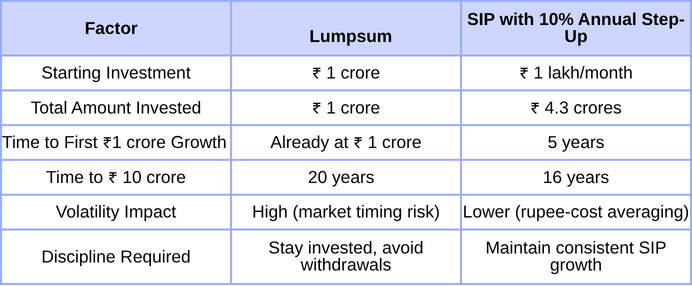

The dream of building a ₹10 crore portfolio is shared by many investors. With India’s equity markets offering long-term growth potential, this goal is certainly achievable with discipline and smart planning. The journey, however, depends greatly on the investment approach you choose. Let’s explore two popular strategies—a one-time lumpsum investment of ₹1 crore versus a systematic investment plan (SIP) of ₹1 lakh per month, increasing 10% annually—assuming a 12% annual growth rate.

The Lumpsum Journey: Slow at First, Rapid Later

If an investor starts with a ₹1 crore lumpsum, the first crore is already in place. At 12% compounded annually, the portfolio grows without additional contributions. Interestingly, the time taken to add each subsequent crore keeps shrinking dramatically as compounding gathers momentum.

The portfolio doubles from ₹1 crore to ₹2 crore in 6.12 years.

Going from ₹2 crore to ₹3 crore takes only 3.58 years.

By the time the corpus grows to ₹9 crore, the final leap to ₹10 crore takes just 11 months!

This acceleration happens because the growth now comes from returns on previous returns—classic compounding in action. The last crore is built almost effortlessly, while the early stages demand patience.

The SIP Route: Slow and Steady Wealth Building

Now, let’s consider the SIP strategy. The investor begins with ₹1 lakh per month and increases contributions by 10% annually.

After 5 years, the corpus reaches ₹97.5 lakh, just shy of the first crore.

By year 10, it crosses ₹3.3 crore.

By year 15, the wealth builds to ₹8.6 crore, and

By year 16, it surpasses ₹10 crore.

The SIP journey is slower initially because the amounts invested are smaller. However, as the SIP amount increases each year and compounding kicks in, growth accelerates significantly. This approach suits investors who don’t have a large lump sum to deploy upfront but can commit to regular, rising contributions.

Key Comparison

Both strategies can lead to a ₹10 crore portfolio, but they cater to different investor profiles. The lumpsum investor benefits from sheer compounding power, watching the portfolio snowball over time. However, this approach carries higher volatility risk. Staying invested without panic is crucial. Amount invested is ¼ of a top-up SIP investor.

The SIP investor, on the other hand, builds wealth gradually while mitigating timing risk through rupee-cost averaging. The annual 10% step-up adds a powerful kicker, ensuring contributions grow alongside income.

Ultimately, the choice depends on the investor’s financial situation and risk appetite. Those with a large sum ready and a long horizon can consider lumpsum investing, while most individuals will find a step-up SIP more practical and psychologically comfortable. Regardless of the path, the key is discipline, patience, and staying invested to let compounding do its magic on the journey to ₹10 crore.