Rohit and Neha, a financially aware couple in their early 40s, were planning to upgrade to a larger home in Mumbai. They had identified a property worth ₹5 crore and were evaluating how to structure the purchase efficiently without disturbing their long-term investment portfolio.

Over the years, they had built a sizeable corpus in equity mutual funds. Their current holding was worth ₹5 crore, of which approximately ₹2.25 crore represented long-term capital gains. Naturally, the concern was taxation. If they redeemed the entire amount, the gains above ₹1.25 lakh would be taxed at 12.5% under Section 112A of the Income Tax Act, resulting in a significant tax outflow.

Instead of viewing this as a cost, they approached it as a planning opportunity.

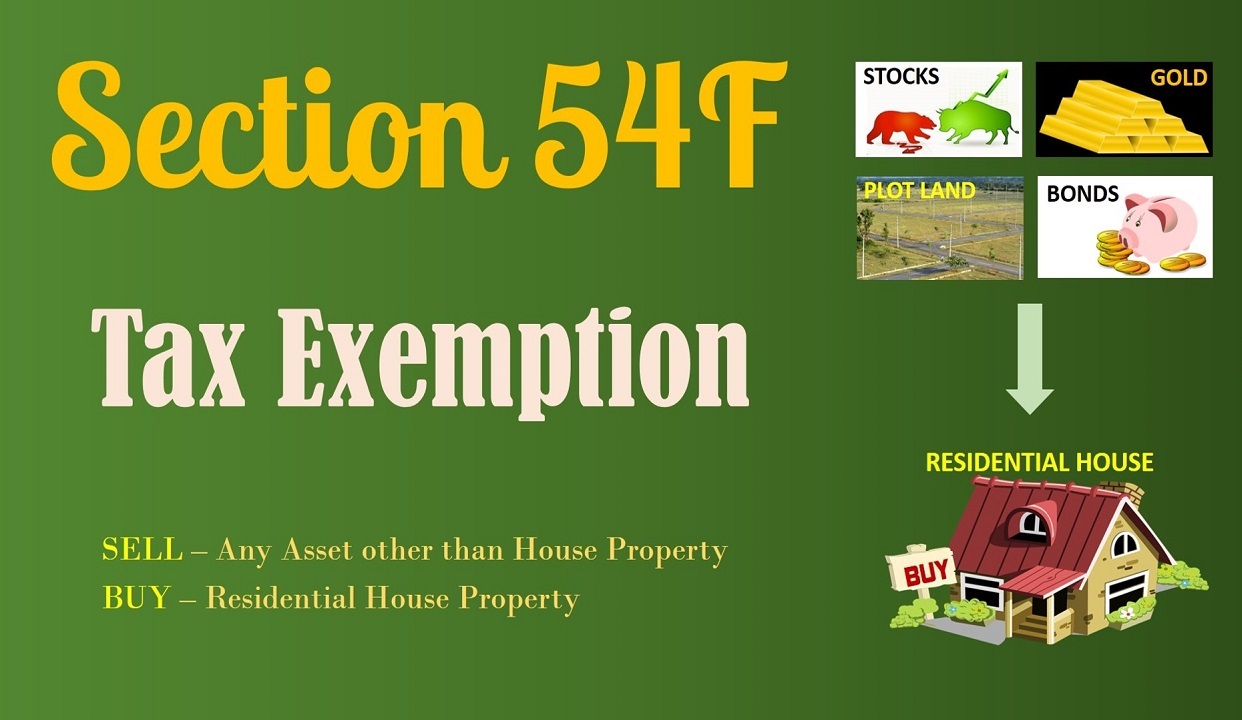

After consulting Team Arthashastra, they structured the transaction in a way that allowed them to legally save 100% of the capital gains tax. They utilised Section 54F of the Income Tax Act, which allows exemption on long-term capital gains arising from assets other than residential property, if the net sale consideration is invested in purchasing a residential house, subject to certain conditions.

Here is how they executed the strategy.

Rohit and Neha redeemed their mutual fund investments worth ₹5 crore. This triggered long-term capital gains of ₹2.25 crore. However, instead of using this entire amount directly for the property purchase, they structured their funding smartly.

They used ₹1 crore from their recent bonus as part of the property purchase and took a home loan of ₹4 crore. The entire property was thus funded through a combination of loan and savings, while keeping the redemption proceeds available for reinvestment.

Since Section 54F requires investment of the net consideration, they ensured compliance by purchasing the residential property within the stipulated timeline. This allowed them to claim full exemption on the ₹2.25 crore capital gains.

Simultaneously, after completing the transaction, they reinvested the ₹5 crore proceeds back into mutual funds, thereby continuing their long-term wealth creation journey without significant disruption.

This structure delivered multiple benefits.

First, they saved the entire capital gains tax on ₹2.25 crore by correctly using the provisions of Section 54F.

Second, by opting for a home loan instead of using the entire proceeds upfront, they maintained liquidity and continued market participation. This ensured that their long-term financial goals, such as retirement and children’s education, remained on track.

Third, they became eligible for home loan tax benefits under Sections 80C and 24(b)—principal repayment up to ₹1.5 lakh and interest deduction up to ₹2 lakh annually, subject to applicable conditions. This added another layer of tax efficiency to the overall plan.

It is important to note that such strategies require careful execution. Conditions under Section 54F include restrictions on owning multiple residential properties and timelines for investment. Proper documentation and compliance are critical.

The key takeaway from Rohit and Neha’s case is that tax planning is not about avoiding taxes—it is about structuring decisions intelligently within the framework of the law.

By combining investment discipline with informed planning, they not only upgraded their lifestyle but also preserved and continued to grow their wealth.

In personal finance, the right strategy often lies not in what you do, but in how you do it.