For most families, taking a loan is one of life’s biggest financial commitments. Whether it is a home loan, business loan, or education loan, it is usually taken with optimism and long-term aspirations in mind. A new house represents stability, a business loan represents growth, and an education loan represents opportunity. But behind every loan lies one important reality—the repayment responsibility depends largely on the earning member of the family.

This is exactly why term insurance becomes not just important, but essential.

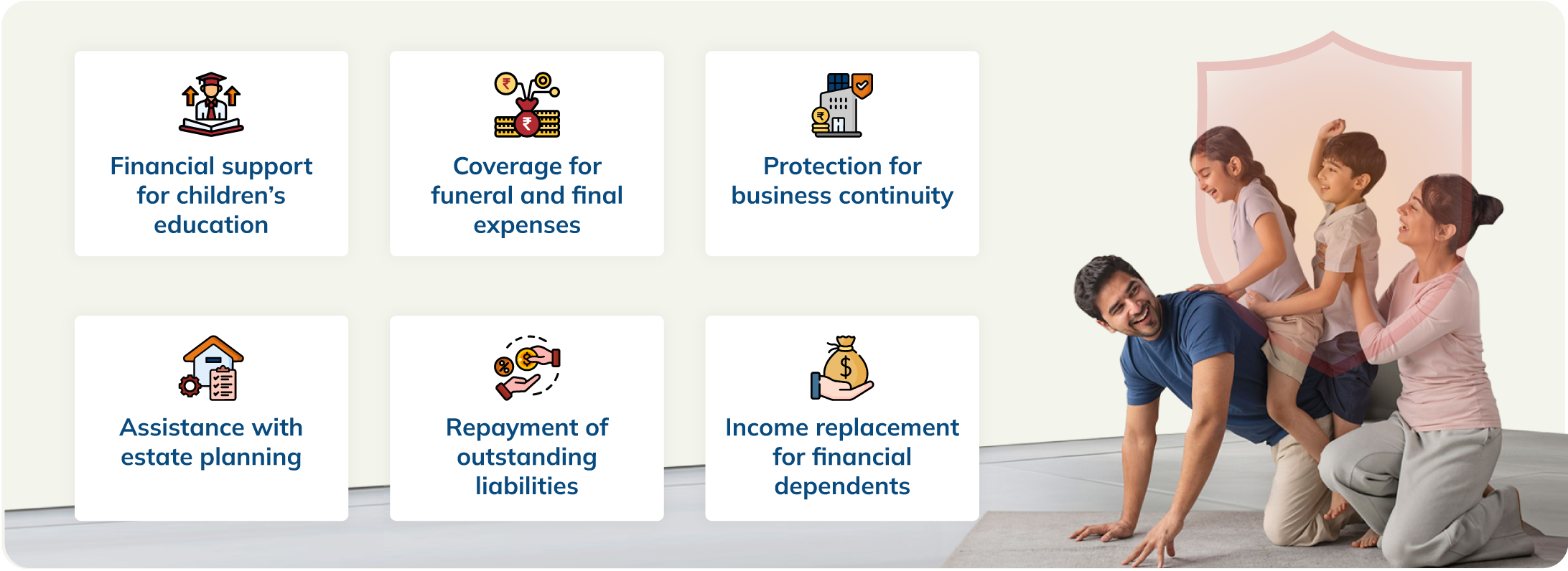

A term insurance policy is one of the simplest forms of financial protection. It provides a large life cover at a relatively affordable premium for a specified period. In the unfortunate event of the policyholder’s death during the policy term, the nominee receives the sum assured. When a family has an outstanding loan, this payout can become the financial shield that protects loved ones from emotional loss turning into financial crisis.

Imagine a family with a ₹1.5 crore home loan and EMIs running for the next 20 years. The house may legally belong to the family, but practically, it remains tied to the repayment ability of the breadwinner. If something unfortunate happens to the earning member, the family is not only coping with emotional trauma but also the pressure of continuing EMIs. Without adequate life cover, they may be forced to liquidate savings, compromise on children’s goals, or in extreme situations, even sell the house.

A properly structured term insurance plan ensures that this burden does not fall on the family. The claim amount can be used to repay the outstanding loan immediately, allowing the family to retain the asset and continue life with greater financial stability.

What many people overlook is that term insurance offers not just protection after an eventuality, but peace of mind during the loan tenure itself. Knowing that one’s family will not inherit debt brings tremendous psychological comfort. Financial planning is not only about wealth creation; it is equally about risk management.

Another common mistake borrowers make is relying solely on insurance offered by lenders along with loans. While loan protection covers can be useful, they are often limited to the loan amount and reduce over time as the outstanding loan decreases. A standalone term insurance policy, on the other hand, can provide broader financial security by covering both liabilities and future family expenses.

Importantly, term insurance should ideally be purchased early. Younger individuals generally get lower premiums, and buying early also reduces the risk of health-related exclusions later.

It is equally important to disclose all health and lifestyle details honestly while purchasing the policy. Insurance works on the principle of utmost good faith, and transparency helps avoid complications during claims.

Loans are taken with dreams in mind, but responsible financial planning requires preparing for uncertainties as well.

In the end, a loan without a term plan is like driving without a seatbelt. You may never need it—but if life takes an unexpected turn, it can protect everything your family has worked hard to build.